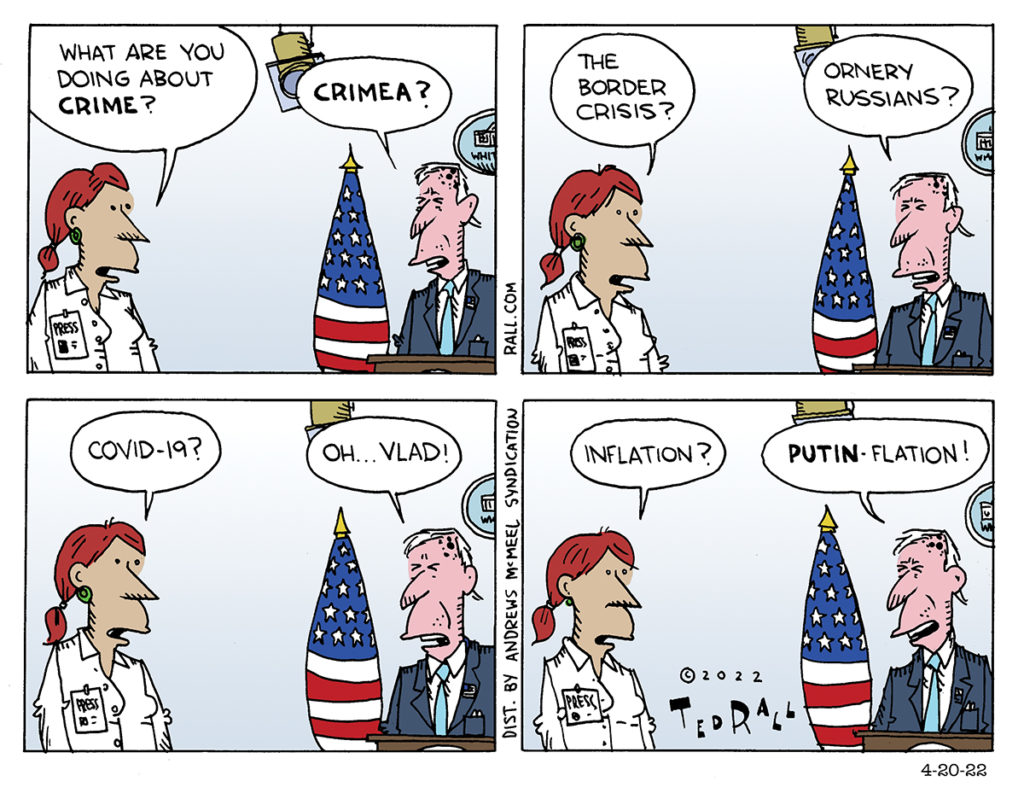

From gas prices to inflation, President Joe Biden is determined to blame Russia for everything that’s going wrong — even stuff that happened before Russia invaded Ukraine.

From gas prices to inflation, President Joe Biden is determined to blame Russia for everything that’s going wrong — even stuff that happened before Russia invaded Ukraine.

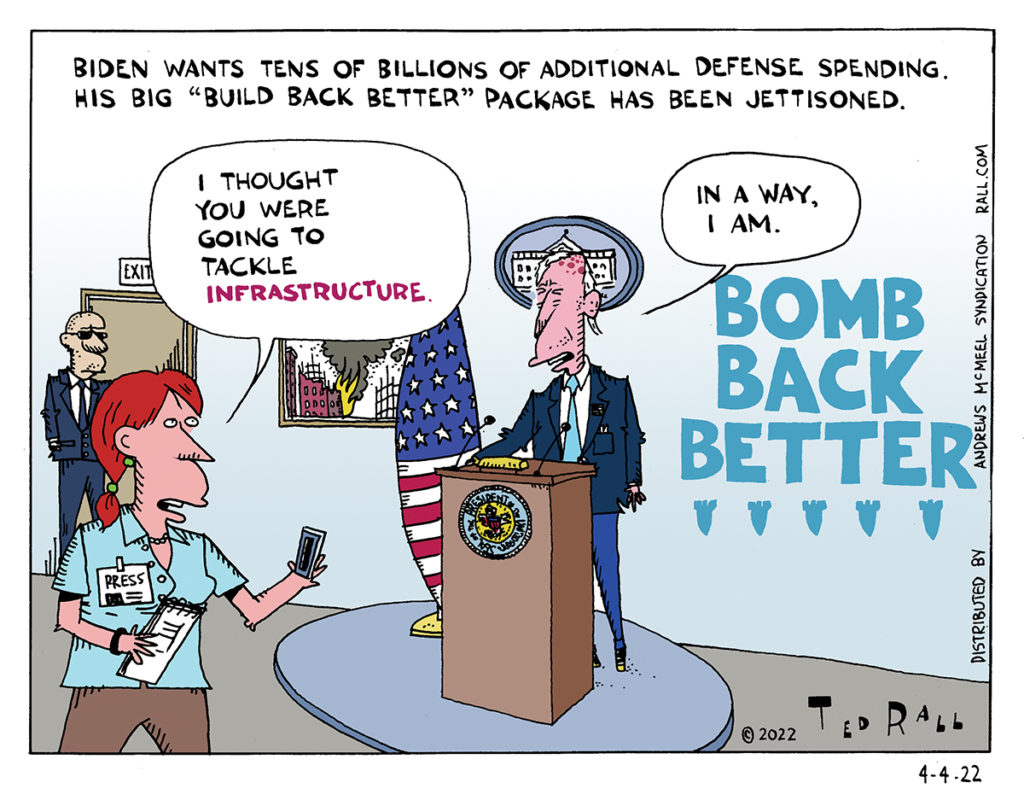

The Build Back Better policy package was supposed to be the centerpiece of the Biden administration’s infrastructure-centered agenda. But now it’s dead because conservative Democrats won’t support it. So the new White House budget doesn’t include it but it ramps up defense spending by billions of dollars.

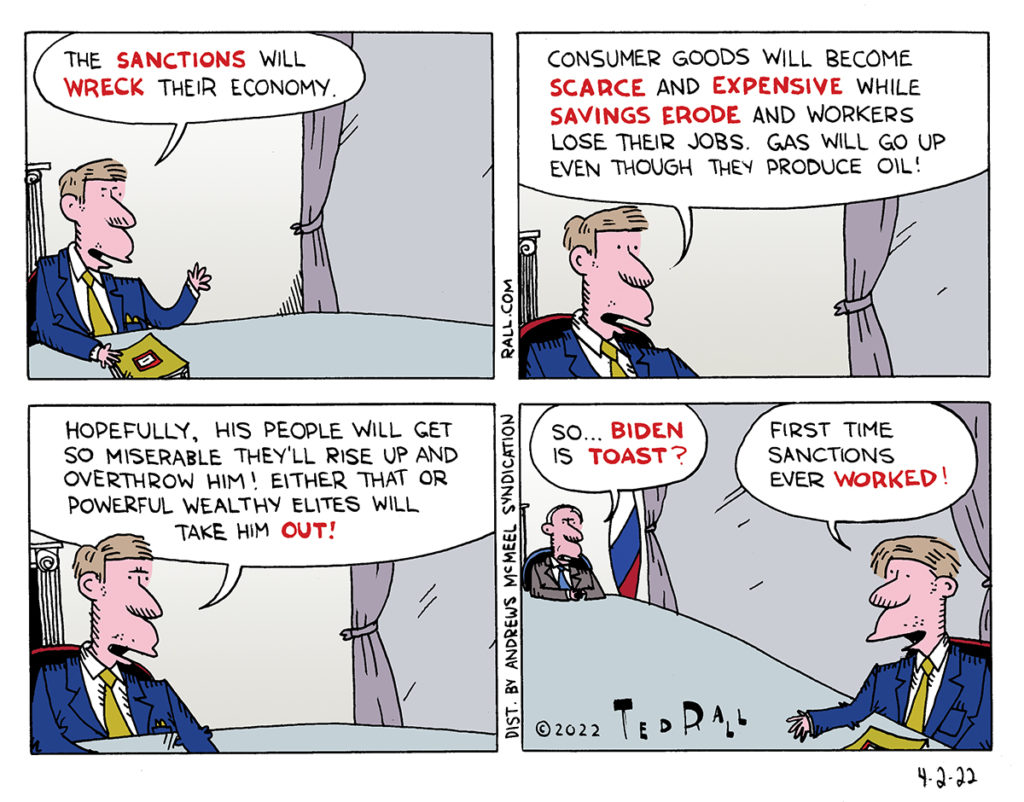

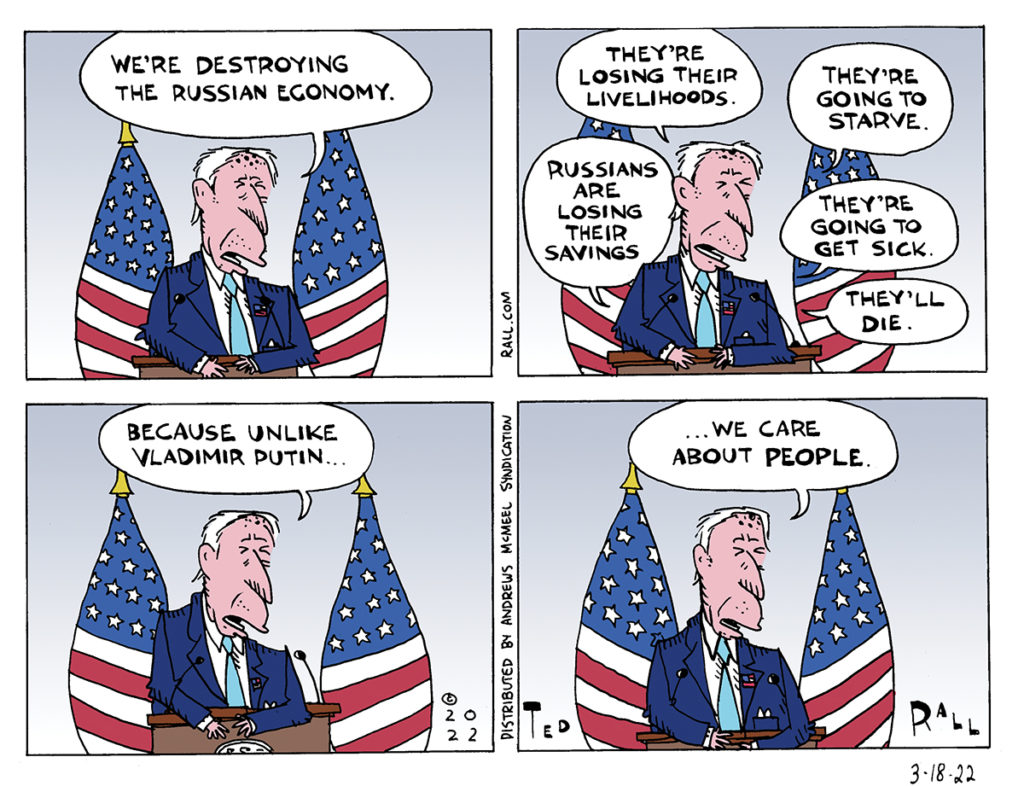

Western nations including the United States have imposed brutal sanctions against Russia in an effort to derail its economy. However, the world is so interconnected and dependent on Russian energy that these countries are shooting themselves in the foot. Effectively, the sanctions are against ourselves.

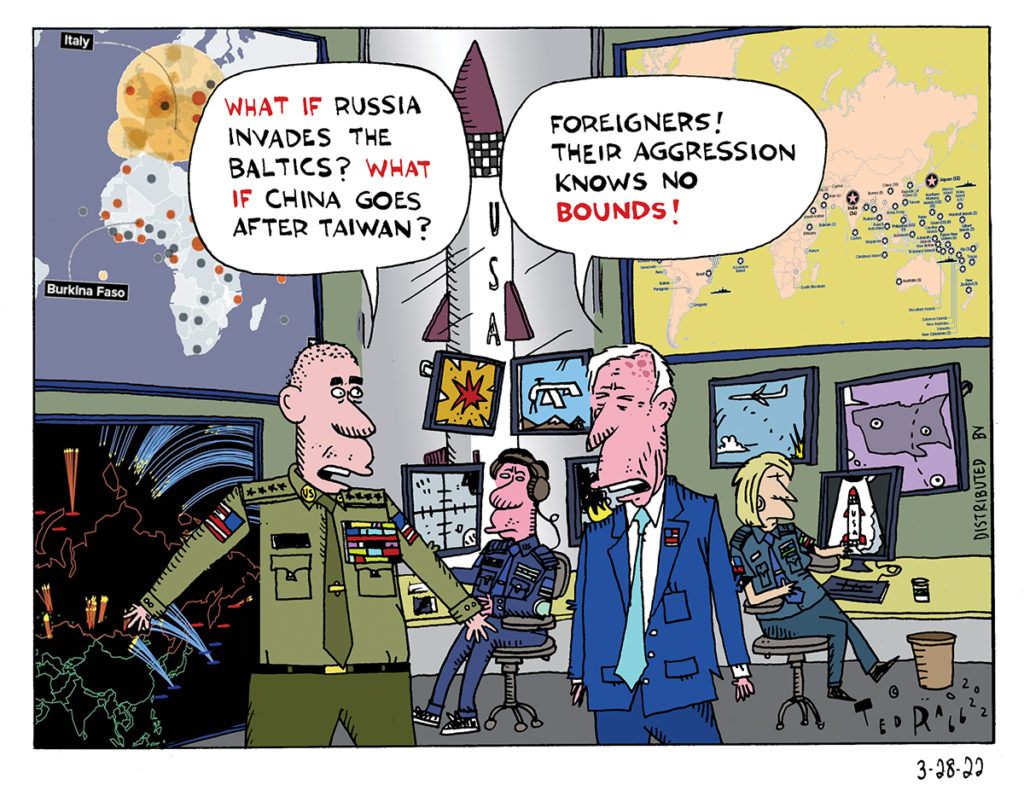

Russia’s invasion of Ukraine has prompted American political leaders and media outlets to constantly speculate about other countries’ military aggression, whether it be the possibility that China would invade Taiwan or that Russia would next turn to the Baltic states. Rarely do they ever consider the fact that they themselves live in the most militarily aggressive country in the world, and that the world should be more afraid of us than we should be afraid of them.

Even the wars that historians judge to have been noble and beneficial rely on popular support marketed and sustained by lies. Contrary to what the English government told its people during World War I, German soldiers didn’t bayonet Belgian babies in their cribs. The “cocaine” U.S. troops claimed to have found in Panamanian dictator Manuel Noriega’s home was nothing of the sort. The Taliban offered to turn over Osama bin Laden – it was George W. Bush who refused to take him, because to accept would have denied him his excuse to invade Afghanistan.

As General and Director of British Military Intelligence John Charteris observed after World War I, “to make armies go on killing one another it is necessary to invent lies about the enemy.”

America’s incipient proxy war against Russia over Ukraine is no exception to the rule. BS has been flying fast and furious as media outlets dutifully align behind the U.S. government war machine and the array of defense contractors that influence it. As usual, their purpose is clear: spook the American people into supporting a war in a country they hardly know anything about, take the side of a highly problematic regime and create a world of death and destruction for the benefit of greedy warmongers before the rubes/voters figure out they’ve been conned.

Let’s take a look at some of the biggest lies being used to garner and prop up support for the Ukrainian government of President Volodymyr Zelensky:

Lie #1: Ukraine is a democracy.

Zelensky won the presidency in a fair election in 2019. But context is critical. The 2019 election was held in the immediate aftermath of a brutal coup d’état. In 2014 a violent mob comprising neo-Nazi extremist groups like the Azov Battalion and Right Sector, and covertly supported by the Obama Administration, forced President Viktor Yanukovych, democratically-elected and pro-Russian, to flee for his life.

The new revolutionary government held an election in 2014, which Petro Poroshenko won. Zelensky is Ukraine’s second post-coup ruler.

Here’s an analogy for Americans: instead of failing, Trump’s January 6th coup succeeds. Biden flees to Canada and, even though he lost, Trump serves a second term. Trump endorses Mike Pence in 2024. Pence wins that election. Is Pence a legitimate president? Is America a democracy?

Democrats would answer no.. As do the 49% of Ukrainians, including many ethnic Russians, who voted for Yanukovych. They feel the same way about Zelensky, that he’s not legitimate. Which is why ethnic-Russian areas in the eastern Donbas region, Donetsk and Luhansk, declared independence and broke away from Ukraine after the 2014 coup, and ethnic-Russian Crimeans greeted Russian forces when they annexed the peninsula.

To half its people, Ukraine doesn’t feel like a democracy.

Lie #2: Ukraine is a free society.

Ukraine is an authoritarian state with a veneer of democracy. Zelensky recently signed a decree ordering that all TV broadcasters in the country show the same exact government-controlled programming on every channel. “It’s important that the country has a unified information policy” under martial law, read the edict. This followed his banning of 11 rival political parties, threatening “a tough response” to politicians who disagree with him.

Lest these repressive measures be excused as regrettable wartime excesses, Zelensky also banned three “pro-Russian” TV channels a year before Russia’s invasion “in order to protect national security,” his spokesperson said. An opposition politician and ally of the stations’ owner was locked under house arrest and accused of treason. Anti-government protesters in Zelensky’s Ukraine are brutally beaten and jailed. In May 2021 the mayor of Kiev said that Zelensky sent thugs from the Ukraine state security agency SBU to his apartment, where they demanded that he toe the line of Zelensky’s policies or else.

“U.S. officials have long been fond of portraying Ukraine as a plucky democracy fending off the menace of aggression from an authoritarian Russia,” Ted Galen Carpenter of the libertarian Cato Institute wrote in 2021, before the war. “Washington’s idealized image has never truly corresponded with the murkier reality, but the gap has now become a chasm.”

Lie #3: Ukraine is an ally that we have an obligation to defend.

If Ukraine were a member of NATO, the United States would have a duty to defend it against Russia. But important members of the alliance like France and Germany oppose Ukrainian membership because it is riddled with corruption and not a full-fledged democracy. “In a 2020 analysis, Transparency International, an anticorruption watchdog, ranked Ukraine 117th out of 180 countries on its corruption index, lower than any NATO nation,” according to The New York Times.

Ukraine is not a U.S. ally. It is in Russia’s sphere of influence every bit as much as Canada and Mexico are in ours. We have no historic or cultural ties to Ukraine.

We have no legal or moral obligation whatsoever toward Ukraine.

Lie #4: Russia’s attack was unprovoked.

I’m not going to endorse Russia’s invasion. But arguing that the move was unprovoked is ridiculous. Ukraine wants to join the EU and NATO, a Cold War-era relic formed as a U.S.-led military counterbalance to Russian influence in Europe. Ukraine has been shelling the Donetsk and Luhansk breakaway regions for years, killing an estimated 14,000 people, mostly ethnic Russians. Not only is Ukraine on Russia’s border, it’s the same exact route Nazi Germany took to invade the Soviet Union during World War II. Ukraine is Russia’s most vulnerable border — and it wants to join a heavily armed, nuclear-capable alliance of states determined to destroy Russia.

Imagine, if you can, Mexico trying to join a Russian-led military alliance. How would we respond?

Lie #5: The neo-Nazi thing is overblown Russian propaganda.

Zelensky is Jewish; he lost family members in the Holocaust. How, goes the argument that concerns about right extremism are mere disinformation, could Ukraine and its government be heavily influenced by neo-Nazism? Well, Barack Obama was Black. Why is the American police still full of racists? Because the president of a country can only do so much. He governs the country he inherits, not the one he wants.

Ukraine has a long and infamous history of far-right politics in which Nazism and anti-Semitism play a starring role. While it’s true that Europe and the United States also have such nasty groups, no other country in the world has as many as a percent of the population. None legitimizes Nazism and fascist collaboration during World War II the way that Ukraine does. “Ukraine is erecting new plaques and monuments to Nazi collaborators on a nearly weekly basis,” The Forward reported last year. Stefan Bandera, a notorious Nazi collaborator, is a national hero with numerous statues in his honor. France had Pétain and Norway had Quisling, but both are officially condemned.

And certainly no other country in the world has police and soldiers openly serving as Nazis, drawing government paychecks while wearing swastikas and other fascist insignia on duty.

Most Ukrainians, arguably an overwhelming majority, are not pro-Nazi. However, an overwhelming majority of Ukrainians, including Zelensky and his government, are highly tolerant — to an obnoxious, intolerable degree — of Nazis serving openly in parliament, controlling a substantial portion of the police and national guard as well as the military. They allow neo-Nazis to control the historical narrative of their country, even elevating traitorous anti-Semites to founding heroes who deserve statues in the streets of major cities.

Lie #6: We have to do something.

It’s a big world. Misery abounds. At any given time there are invasions, proxy wars, regional conflict, civil strife and illegal occupations on almost every continent. Yemen is on fire. The Israeli-Palestinian conflict grinds on. Afghanistan is starving. Those are three cases where the United States is involved, as usual on the wrong side. There are dozens of other conflicts in which the United States has little to no interest. The only reason we are involved in Ukraine is because the media tells us to be.

It is entirely reasonable to look at the conflict between Russia and Ukraine and decide that it’s simply not our business, that neither side is worthy of support.

(Ted Rall (Twitter: @tedrall), the political cartoonist, columnist and graphic novelist, is the author of a new graphic novel about a journalist gone bad, “The Stringer.” Order one today. You can support Ted’s hard-hitting political cartoons and columns and see his work first by sponsoring his work on Patreon.)

What if Joe Biden were to admit to Vladimir Putin the obvious truth, that the United States is an expert in all the acts of villainy Russia is committing and accused of in Ukraine? What if he warned Russia that it would suffer the same loss of credibility United States has in criticizing Russia?

American politicians and television viewers have been deeply moved by images of the suffering people of Ukraine. Unfortunately, the main response has been to impose brutal sanctions on Russia that will destroy the Russian people but not their leaders, who are well insulated from the effect of sanctions. If humanitarianism is the point here, what about the people, the human beings, of Russia?

It is virtually inconceivable that Ukraine will be able to defeat Russia militarily. Russia is simply too powerful. So what’s the point of sending weapons to Ukraine? There can only be one net effect, to prolong the war and the suffering to the benefit of the defense industry.

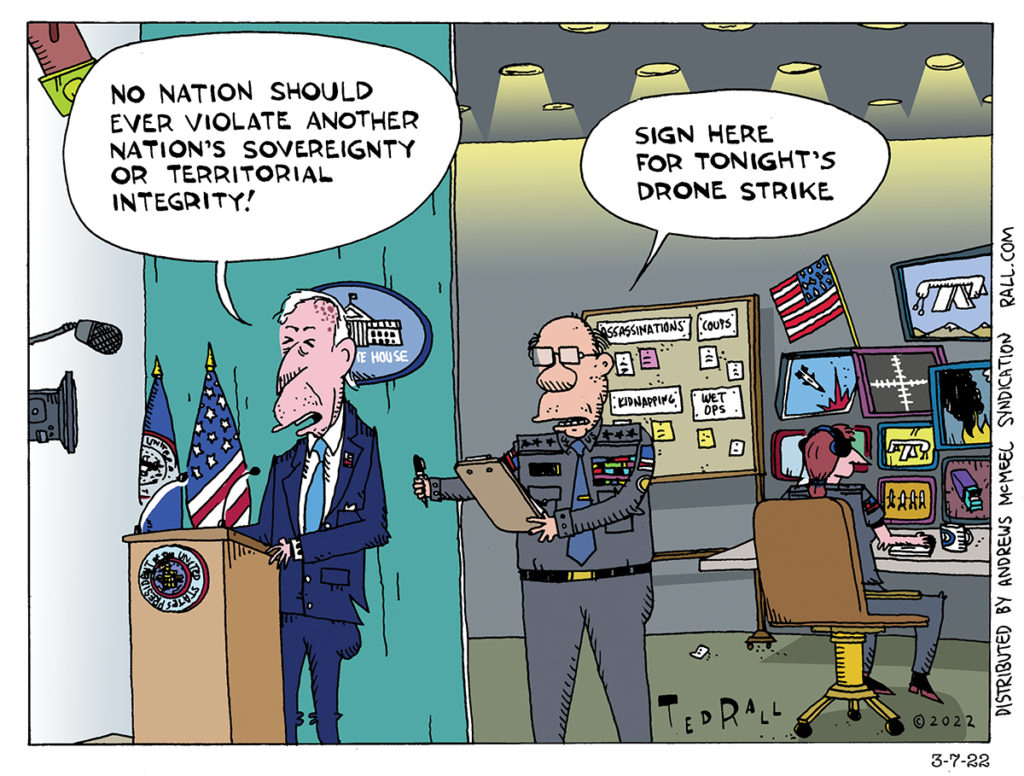

Joe Biden and the media outlets that support the Democratic narrative support Ukraine against Russian invasion without pausing to consider the fact that the United States is by far the biggest interventionist power in modern history. A nation that carries out drone strikes, assassinations, covert coups d’état and massive invasions and occupations of countries all over the planet has no moral standing to complain about the actions of any other country.

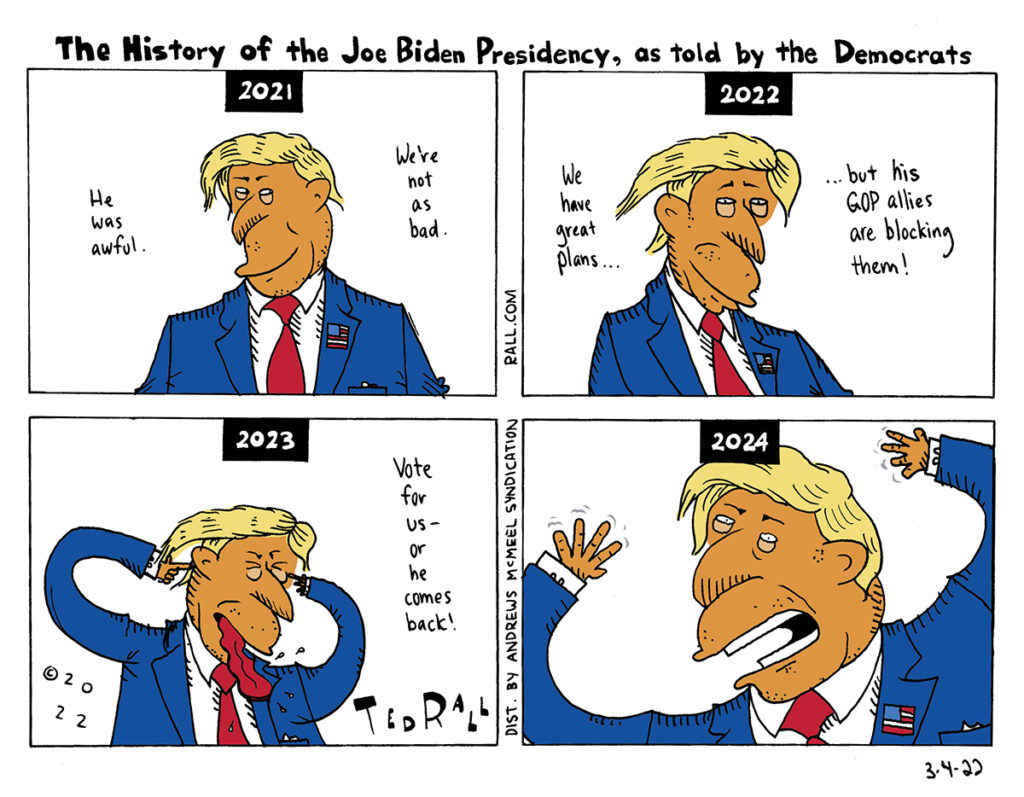

The dumbest thing you can do in politics is to fall into the framing of the opposite party. But that’s exactly what the Democrats are doing by constantly comparing President Joe Biden and congressional Democrats to former President Donald Trump and his allies.