What would get people to go back into stores? Indeed, shoplifting is up nationwide.

Chronicling the end of the empire is fun.

What would get people to go back into stores? Indeed, shoplifting is up nationwide.

Chronicling the end of the empire is fun.

Soak the Rich, Corporations

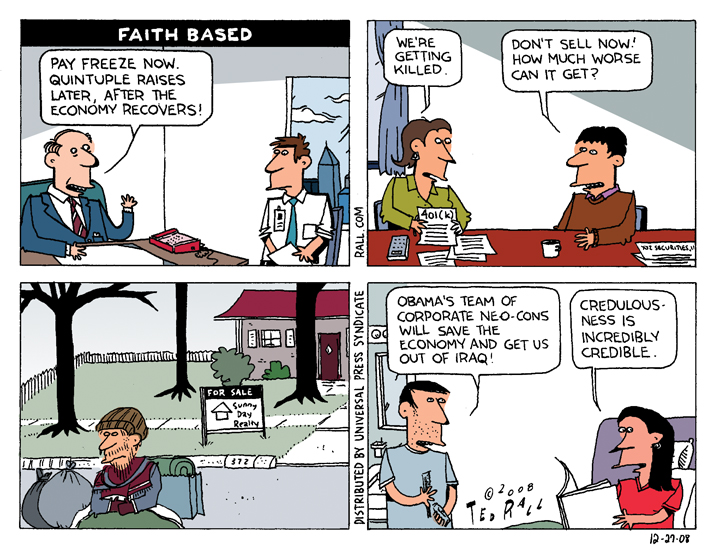

A moratorium on housing foreclosures and evictions is a good idea. So is making the tax code more progressive. Obama’s plan to build new public works is smart. But those are half-measures. Even if they don’t come out of Congress watered down and wankified, they’ll come too little and too late to kill the rapidly metastasizing disease that threatens to kill the U.S. economy: income inequality.

Employers are shedding jobs at a breathtaking rate: more than 560,000 per month. The rate of job losses could soon hit a million. People who still have jobs are being squeezed by pay cuts and freezes; even those who have yet to be affected are closing their wallets out of fear that they’ll be the next to get chopped. So consumer spending, which accounts for two-thirds of economic activity, is plunging. Moreover, millions of individuals and businesses have lost access to credit and thus the movement of capital that might have pulled us out of this tailspin.

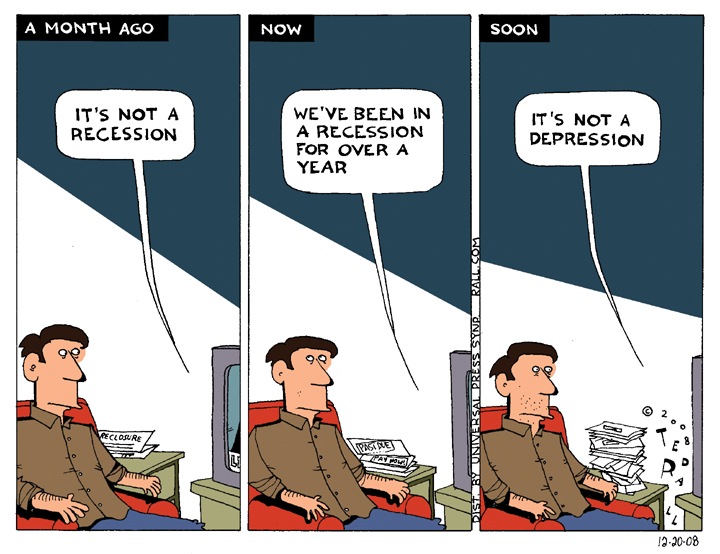

“The key is that the consumer is in the worst condition since the Great Depression,” retail consultant Howard Davidowitz told NBC News. Boarded-up shops will abound. Experts expect 73,000 retail locations to close during the first few months of 2009. Between 20 and 40 percent of national retail chains will shut down. This isn’t a recession. It’s a depression, and it could destroy the country.

If broke consumers are the problem, shoveling money into their pockets is the way to get them spending again. Where do get it? The reason Willie Sutton robbed banks, he supposedly said, was because “that’s where the money is.” These days, the money is the hands of corporations and rich individuals.

(Warning: boring economic statistics and analysis follow. But stick with me. You could get a check!)

Tax returns give only a partial picture of a nation whose riches have been aggregated in the hands of a tiny elite. “The Internal Revenue Service,” reported The New York Times in 2007, “captures only about 70 percent of business and investment income, most of which flows to upper-income individuals, because not everybody accurately reports such figures.” So actual income inequality is bigger than IRS data indicates.

Even so, the IRS finds a huge pay gap between the very rich and the rest of us. “The wealthiest one percent of Americans earned 21.2 percent of all income in 2005,” the most recent year for which IRS data is available, according to a 2007 piece in The Wall Street Journal.

What if we played Karl Marx and left that one percent of the population (people who earn over $350,000 a year) with their fair share–one percent of national income? If we divided the rest of the loot equally, everyone else–99 percent–would get a 20.2 percent pay raise.

I don’t know about you, but I could use it. And because I’m a patriot, I pledge to fritter away half of my 20.2 percent windfall on wine, women and frivolous American-made consumer goods.

What would happen if we adopted the communist principle of total income equality? That would require closing the gap between median (the halfway mark of income distribution) income and average income. Due to wage inequality, the average worker earns 40 percent more than the median. Close the gap, and two-thirds of Americans get a raise. One-third gets a cut. But only a small group, the top five or ten percent, would feel significantly pinched. Most of the third wouldn’t lose much. And everyone would benefit from the increased economic activity that would result from equal income distribution.

Call it trickle-up economics.

Wouldn’t socialism remove people’s incentive to work hard? Though not a perfect economic model, the Soviet experience seems to disprove the idea that you can’t find good CEO help for under a million bucks a year. Soviet physicists, athletes, filmmakers, novelists, composers and other innovators led their fields, yet were rewarded with little more than a medal and a puff piece in Pravda. Mikhail Kalishnikov invented the AK-47, the world’s most popular firearm. He was never paid a dime, and never cared.

Here in the U.S., brilliant people become schoolteachers and priests. Salary isn’t the biggest motivation for most people.

Another thing to bear in mind is an aspect of wealth Americans don’t usually think about: assets. Eliminating income inequality wouldn’t address asset inequality. The rich, who’ve had years of high income with which to save and invest, and have inherited assets from parents and grandparents who did the same, would still be rich. A truly efficient attempt to put more money in the average person’s pocket would require redistribution of these accumulated assets.

If Willie Sutton were still around, however, he might find it easier to go after biggest 4000 U.S. corporations than its richest 40 million households. So let’s look at big business income.

After-tax 2007 profits for U.S. corporations totaled $1.8 trillion, up 10 percent since 2001. (Bear in mind: this figure doesn’t include CEO salaries, capital reinvestments, and the acquisition price of other corporations.) The effective average corporate tax rate in the U.S. is about 13 percent–one of the lowest in the industrialized world. If we were to double the effective tax rate to 26 percent, the U.S. would remain a tax haven compared to Germany and other major European countries.

Let’s say the IRS took that extra 13 percent corporate profits tax and cut a check to the American people. Why not? Without us, the U.S. consumer, these companies wouldn’t be in business. In 2007, every worker in the U.S. would have gotten a check for $12,000. That’s a lot of xBoxes, not to mention mortgage payments.

There’s plenty of cash left in the U.S. economy. Sooner or later, the tiny minority of corporations and rich individuals who are hoarding our nation’s wealth will be forced to share it with the rest of us. The question is when, and how.

COPYRIGHT 2009 TED RALL

It’s true: for the first time in memory, all three TV networks have pulled all of their full-time reporters out of active war zone: Iraq.

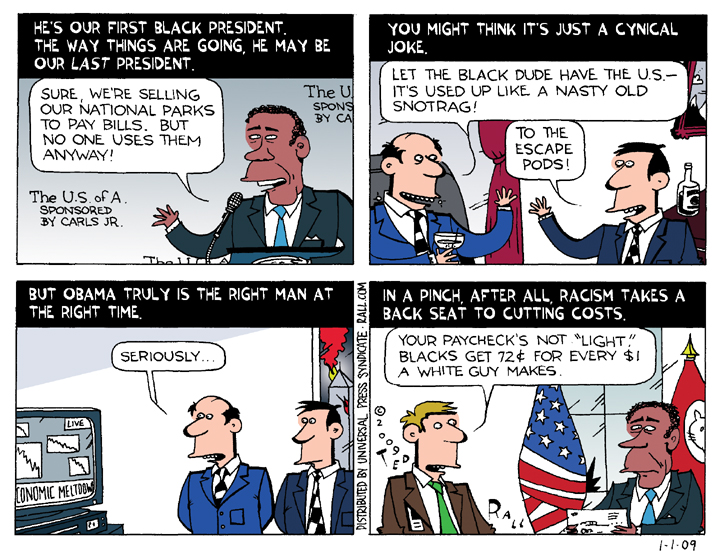

Now that the U.S. is used up like an old crumpled piece of tissue paper, they hand it over to a black guy.

There’s Plenty of Money Around. Let’s Take It.

What’s the difference between you and a corpse? You both contain the same organs, the same fluids–all the same stuff. Inside you, stuff moves around. That’s the difference between life and death.

What’s the difference between economic boom and bust? Again: movement. The United States of America is just as rich today as it was a year or, for that matter, ten years ago. It still possesses the same rich natural resources, the same enviable geography, and the same productive, innovative and energetic workforce. Our country still has enormous intrinsic value. But money, the lifeblood of any economy, has stopped moving around.

Wealth is still here. But the economy has flat-lined.

We know what caused the problem–the double bursting of the dot-com and housing bubbles, coupled with government regulators who took the last three decades off from work and financial analysts who said the old rules no longer applied. (The old rules always apply.) The underlying meta causes of the Crash of ’08 were an unholy trinity of stagnating wages, easy credit and brilliantly executed consumer propaganda that convinced people they were lame unless they bought all the latest stuff. But that’s a discussion for another time. This week, let’s think about how to escape the deflationary spiral that will reduce the world’s richest nation to penury unless something is done soon.

The Fed, having reduced interest rates to zero, is out of ammo. Banks are using the $700 billion bailout to buy each other up, enriching only themselves and a few hundred investment bankers. (In all fairness, Treasury Secretary Henry Paulson told them to do just that.)

President-Elect Obama’s plan blends George W. Bush and FDR’s greatest hits: a symbolic Bush-style tax cut of $500 per person ($1,000 per couple) and a $850 billion infrastructure construction bonanza reminiscent of the WPA projects of the 1930s. Obama’s tax cut won’t stimulate the economy; they never do. Due to the “multiplier effect,” Obama’s economists predict that his public works projects will create 3.2 million new jobs by the first quarter of 2011. “Peter Morici, economist at the University of Maryland, projects that $100 spent on a bridge or school boosts economic activity by about $200,” reports the Associated Press. (That doesn’t count the benefit of improving Americans’ longer-term productivity. For instance, better roads could reduce commuting times or help get goods to customers more efficiently.)”

A public works program is a good idea. But Obama’s plan won’t be enough to put a dent in the skyrocketing unemployment rate. 3.2 million jobs would be barely enough to replace six months worth of job losses at current rates. And most analysts think those rates will rise. With the federal budget continuing to sink $9 billion a month into the fiscal sinkhole of Iraq, there isn’t much cash to make the plan bigger.

“With negative or low economic growth projected well into the future, the economy needs a long-term fix,” says Stanford economist John Taylor, who worked in Bush’s Treasury Department. Definitely. But what?

Unless something big happens (like every pundit, I should predicate every prognostication with the acronym USH for “unless something happens”), the depression will deepen quickly. Our economy is two-thirds dependent on consumer spending, but consumers are stone cold broke. Decades of attacks on labor and free trade agreements caused wages to stagnate as inflation raged, so Americans have no savings to draw upon. Credit is no longer available as a back-up.

The American consumer has left the building.

Demand will keep shrinking, forcing companies to lay more people off, which will accelerate the shrinkage of their customer bases. Prices will drop to chase the few dollars left in the economy, triggering deflation. It’s already begun: Prices fell 1.7 percent in November (20 percent on an annualized basis). Debtors will try to pay off inflated credit card bills and mortgages with deflated money. They will fail. Misery will spread.

What happens next, I think, is that people will do what large numbers of people always do when they need money and food but can’t find a job. They will start to think about the rich, who still have all the wealth they accumulated while money was still circulating. And they will take it from them. It might be the easy way, through liberal-style income redistribution. Or it might be the hard way. Either way, it goes against the laws of nature to expect starving people to allow a few individuals to sit on vast aggregations of wealth.

When I was young, I assumed that revolutions resulted from ideology, because idealists wanted a fairer world. Now, as we stare down the barrel of economic apocalypse, I realize that they’re carried out by desperate people who have nothing to lose, in Marx’s words, and everything to gain. They take stuff from the rich and write the ideological tracts after the fact.

With the economic distress we’re likely to see in the coming year or two or three, revolution will become increasingly likely unless money starts coursing through the nation’s economic veins, and soon. Will it be a soft revolution of government-mandated wealth distribution through radical changes in the tax structure and the construction of a European-style safety net, as master reformer FDR presided over when he saved capitalism from itself? Or will the coming revolution be something harder and bloodier, like the socioeconomic collapse that destroyed Russia after the fall of the Soviet Union? To a great extent, what happens next will depend on how Barack Obama proceeds in his first weeks as president.

COPYRIGHT 2009 TED RALL

The U.S. can’t find $25 billion to save three million jobs related to the auto industry, yet it keeps shelling out $9 billion a month on Iraq. And Obama will keep it up (see this week’s column).

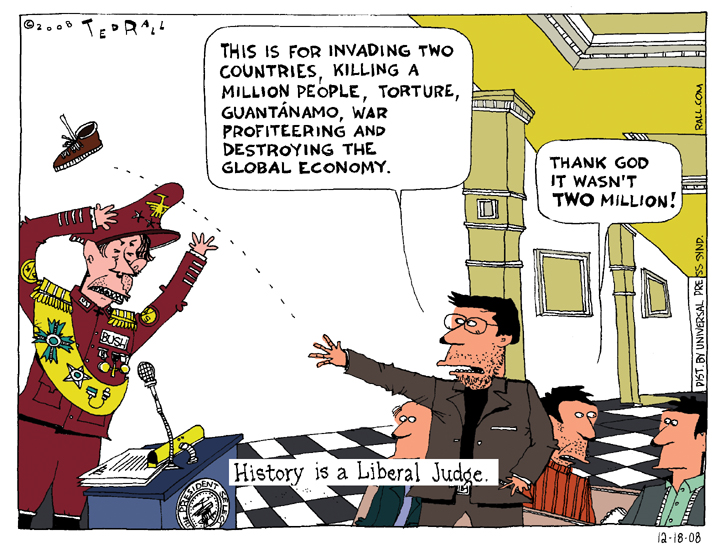

Getting a pair of shoes tossed at him may end up being the only punishment Bush gets. Pathetic.

Stop Speculators From Ruining Strong Companies

The Crash of ’08 offers the incoming Obama Administration a rare chance to rein in the excesses of our economic system. I can think of few better places to start than banning leveraged buyouts.

Leveraged buyouts (LBOs) are Wall Street’s solution to American capitalism’s dirtiest secret and biggest problem: no one has any money. Really. Working as an investment banker during the 1980s, I was repeatedly astonished when deals would fall apart because would-be buyers of major corporations didn’t have enough cash on hand to buy a house in the Hamptons. Many of the wealthiest people in the world, it turned out, have zero or negative net worth. According to The New York Times, for example, one of Donald Trump’s biggest sources of income was his job hosting the TV show “The Apprentice.” Those buildings with his name on them? He leased his name to developers who liked his brand.

It’s true: the rich are different than you and me. But not because they’re rich. If most “wealthy” people ever had to settle up with their creditors, they’d be worth less than the average homeless Iraq War vet. What they do have—or, until recently, had—big lines of credit.

LBOs are a way for cash-poor “rich” people and corporations to buy companies they can’t really afford. First the would-be acquirer buys enough stock to get controlling interest in the targeted company. A bank lends him the rest of the purchase price, using the purchased company’s own assets as collateral. Overnight, a profitable company with a healthy balance sheet can find itself burdened with staggering debt—its own purchase price.

Now the corporate raider owns the company. But the company owes big payments to the bank. The raider has two options. He can use his management skills to make it more efficient and profitable. Or he can sell off pieces of the company. More often than not, “turn around” experts find that they’re not much smarter than the management they replaced and end up selling assets and cutting costs. For other acquirers, turn-arounds aren’t the point. They’re out to gut the joint from the start.

The results are the same in both scenarios. Each sale of a division and each round of layoffs reduces the already cash-starved acquired company’s chances of survival. The formerly profitable company is forced to file bankruptcy. Its employees lose their jobs. Because the law inexplicably lets corporations use retirement plans as collateral for loans, they often lose their pensions too. Suppliers are stiffed. Customers suffer higher costs due to less competition.

It’s bad news for most people—but not for everyone. The corporate raider sells off his equity stake in the company before the fiscal excrement encounter the fan, then pays himself and his friends millions in golden parachutes. The bank, which collected high interest payments as the company began its post-LBO decline, seizes and sells off what remains of the company’s assets.

Here’s another way to look at it: Let’s say you want to buy a car you can’t afford, like a Rolls Royce. You “buy” the fancy hand-crafted auto using the car itself as collateral. When the payments come due, you sell the engine, tires, carburetor, CD player and other parts to a chop shop. You pocket the cash and default on your loan. This, of course, is illegal—yet in this scenario all that’s been lost is a nice car.

LBOs inflict much greater damage. They transform profitable companies into bankrupt ones, throw thousands of people out of work, stifle competition and deprive government of the tax revenues it needs in order to build schools, maintain roads, and drop bombs on Muslims. Yet LBOs are legal.

Generally speaking, LBOs succeed under two conditions: an expanding economy and a management team able to radically increase profits in a short time. These conditions are rarely present at the same time, and almost never for very long.

Signs that the LBO model was untenable began appearing 20 years ago, when two of corporate raider Robert Campeau’s victims, the Revco drugstore chain and Federated Department Stores, went bankrupt. Federated, which employed thousands of American workers before Campeau came along, had been saddled with LBO debt equal to 97 percent of its net assets.

LBO transactions have since led to scores of bankruptcies and hundreds of thousands of Americans losing their jobs—all to line the pockets of a tiny cabal of greedy speculators. The LBO goons’ latest victims, ironically enough, are the media giants lionized by their own business reporters in breathless puff pieces.

In 2007 Sam Zell, described as “a 65-year-old billionaire and president of Chicago-based Equity Group Investments,” bought the Tribune Company for $8.23 billion. Tribune was one of the largest media chains in the United States, owning The Chicago Tribune, The Los Angeles Times, The Baltimore Sun, 20 television stations, and other properties—as well as the Chicago Cubs baseball team. Like most “billionaires,” Zell didn’t have any money. Like most takeover artists, he didn’t know anything about the multibillion-dollar business he wanted to run.

Zell invested a mere $315 million (3.6 percent of the purchase price) and stuck Tribune with $8.4 billion in debt, promising to make early debt payments by selling the Cubs and turning around the company’s flagging newspapers.

Everyone saw trouble ahead. “The leveraged buyout is making Tribune one of the riskiest newspaper companies, according to John Puchalla, a media analyst at Moody’s Investors Service in New York,” reported the Bloomberg business wire service at the time. Now, a year later, Tribune has filed Chapter 11. Layoffs are coming fast and furious. After just 18 months under Zell’s careful stewardship, Tribune—formerly a profitable company—reports assets of $7.6 billion and debt of $13 billion.

“Factors beyond our control have created a perfect storm—a precipitous decline in revenue and a tough economy coupled with a credit crisis that makes it extremely difficult to support our debt,” Zell said, acknowledging the disaster.

Zell is right about the credit crisis. But it would have a lot easier for Tribune to weather the storm if he’d never come along.

COPYRIGHT 2008 TED RALL