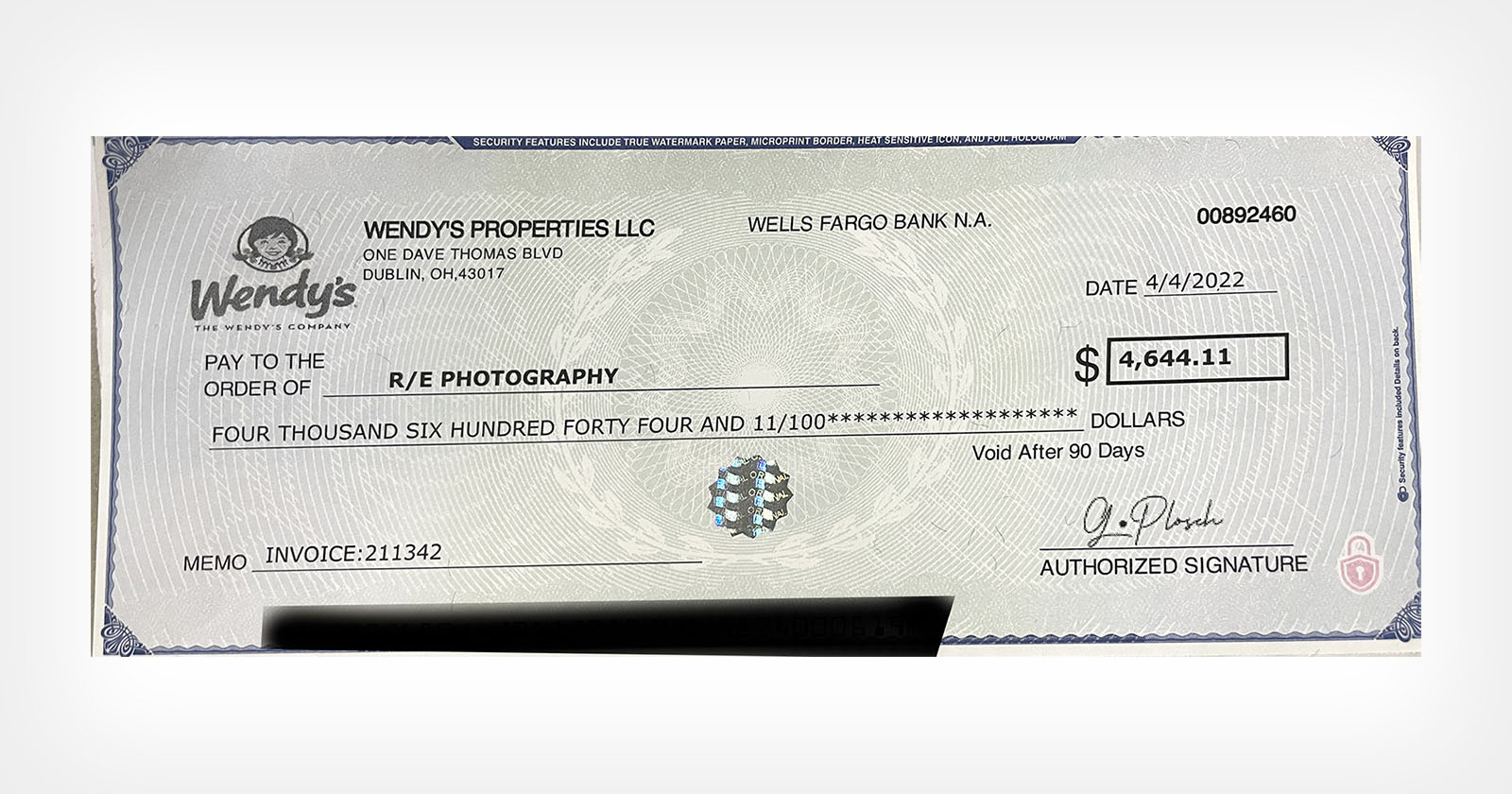

When my landlord’s management company informed me that they hadn’t received my rent check, I was surprised. As for most Americans, housing is by far my biggest expense. So of course I noticed when the money vanished from my account. The mystery deepened when I conjured up an image of the canceled check on my bank’s website. There was my check, canceled and endorsed. I sent a screenshot to my management company.

Look closer, they responded. We didn’t cash it. That’s the signature of some random person—not us.

So it was. How could my bank clear a check for thousands of dollars made out to a company like “XYZ Management Corp.” but endorsed by a completely unrelated individual—one who doesn’t work there, natch—like “John Smith”? What were my rights in this situation? The answers to those two questions provide insight into state of a country that has lost its way.

There is a prequel to the first question: how did the thief access my check?

I mailed the check from the mailbox right in front of my local post office. (This, banks say, is a best practice. Clearly not.) When I inserted the envelope, the slot felt weird. I shoved it in as much as I could but I wasn’t sure it went all the way in. Turns out there is a “mail fishing” scam where miscreants put something sticky at the opening of the mailbox and scoop out items like my rent check. It’s one thing to try something like that on a box in the middle of nowhere but here we’re talking about a box a few feet from the door to a Manhattan post office. When thieves are this brazen, law and order is breaking down.

Adding insult to injury is the fact that the USPS made mail fishing easier when they replaced the old-fashioned swivel openings up their drop boxes with those with skinny slots, which only take letters, in response to the fear that terrorists like the one who blew up TWA Flight 800 in 1996 would use them to mail package bombs. Actually, neither mail nor terrorists had anything to do with the crash of Flight 800. The impetus for this change was the post-disaster diktat that Postal Service customers could no longer mail items heavier than 16 ounces from letterboxes. The government solved a nonexistent problem and created a new, real one.

Half a lifetime ago, I was a banker. Back in the 1980s, there was no way any bank would clear a check that wasn’t endorsed by the payee. Forgers had to work for their/your money.

Some scoundrels still display good old American ingenuity. They wash your check and change the amount from, say $9 to $9,000, and alter the payee to themselves. But that wasn’t the case with my check. The payee remained the same. The rent was substantial to begin with; besides, when I saw the correct amount of my check go out of my account it didn’t arouse suspicion for weeks, allowing plenty of time for the thief to move my money elsewhere.

The person who stole my check deposited it via a mobile app. Check fraud through mobile banking is costing the banking system over $1 billion a year. And, like mine, many of these bad checks are so poorly executed that any moron who looked at it would flag it. The problem is, no one is looking—only a computer.

You really have to wonder whether this technology is ready for prime time. A 2021 story from Indianapolis is typical: “The type font used to alter the information on the [fraudulent] checks is clearly different than the type used on the rest of each document. And one of the photocopied checks shows the name and address of the original payee were sloppily covered by strips of paper that the perpetrator cut and pasted onto the altered document. As far as con-jobs go, this wasn’t even a good one.” The other culprit is bank executives. Technology that automatically scans for tells like this is available—but it’s more expensive. Those ridiculous bonuses aren’t going to pay for themselves.

A friend in college had a night job clearing checks for a small bank in New Jersey. All the checks went through a scanning machine but the larger sums were personally handled by a human being: Jim. Jim was handsomely paid so, naturally, all the Jims have been replaced by machines. But, like Google AI, the machines don’t do a very good job.

If banks are so allergic to hiring actual people that they’re willing to absorb the resulting cash shrinkage, so be it. But they’re not. They’d rather pass on the cost of the grift to us.

I would name my bank here—but that would only expose me to more bank fraud.

As soon as I became aware that my rent check had been stolen, I got on the phone with customer service. Not only was there no option in the phone tree to report fraud, there was no option to talk to a human being. I hit “0” several times, cursing loudly, and eventually was put through to someone in, I’m guessing South Asia, who had a lovely lilting accent I could hardly understand. She made me understand the bank would mail me an affidavit to sign and return. Which they did, though it contained several major errors. After an investigation, a process that takes months, I may or may not get back my money—which, remember, the bank gave away to some idiot without exercising the slightest iota of due diligence to make sure it was a legitimate transaction. But this should be their problem, not mine. Given that this was 100% their mistake, shouldn’t they have credited my account and gone after the rapscallion themselves? (For the record, I would be happy to testify against this creep in court.)

When the form arrived, I made my way to my local branch where an officer informed me about their hilariously Kafkaesque policy. Closing your account is a major pain, requiring you to notify all your direct depositors and automatic withdrawals of your new account information. But if you refuse, the bank will not consider refunding the lost money unless you sign a form indemnifying them for any and all fraud of any kind in perpetuity. As a worker in the dying field of journalism, I don’t think indemnifying a large transnational bank is smart. Obviously, closing the account is the right move. But if you close your account, the bank said, they have no way to return the stolen money. I asked them to close it anyway—but they can’t due to “pending transactions.” Which won’t clear because the account is blocked.

It’s really quite beautiful, an enigma wrapped in a paradox smeared with poo.

Just another indignity suffered by just a typical consumer in the naked city. And it explains everything that’s wrong with this country: humans replaced by robotic morons, American jobs outsourced to foreign incompetents, systems designed for abuse, security measures that make things less secure, corporations that never accept blame for their mistakes, all the weight of the screw-ups placed on the shoulders of individuals who can’t afford it.

To my landlord: Hopefully I’ll get your/my money back in three months.

(Ted Rall (Twitter: @tedrall), the political cartoonist, columnist and graphic novelist, co-hosts the left-vs-right DMZ America podcast with fellow cartoonist Scott Stantis. You can support Ted’s hard-hitting political cartoons and columns and see his work first by sponsoring his work on Patreon.)