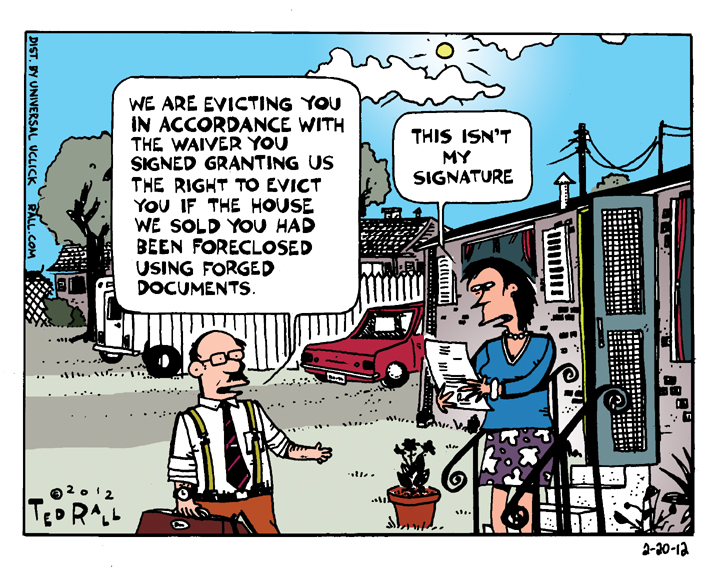

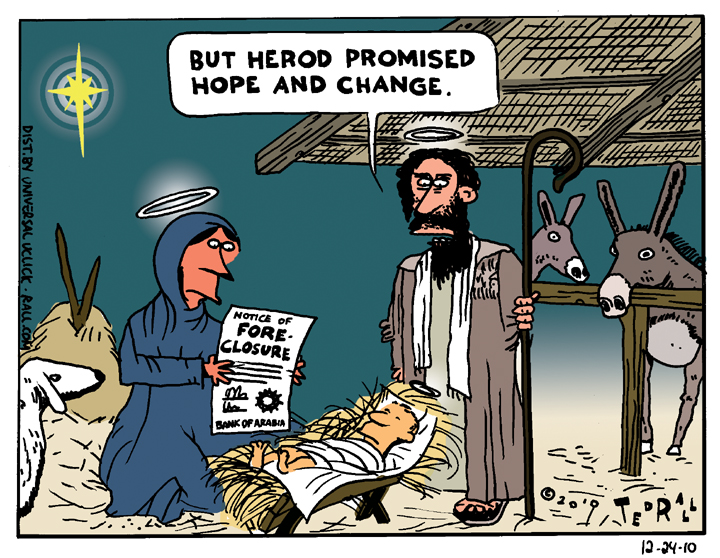

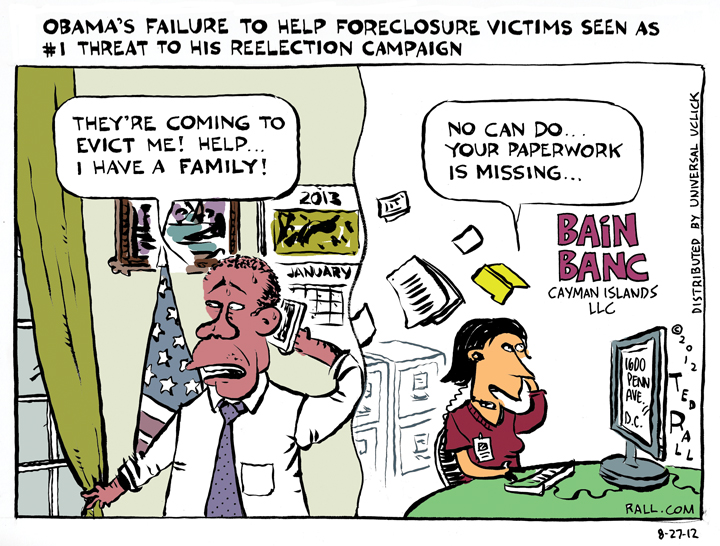

Obama tried to finesse his response to the housing crash, rejecting a bailout of homeowners facing foreclosure in favor of a limited aid program and a bet that a recovering economy would take care of the rest. Millions of people lost their homes and the recovery never materialized. The economy is now the primary threat to Mr. Obamaâs bid for a second term, and economists and political allies say the Obama’s non-response to the housing crisis was the administrationâs most significant mistake.