President Biden’s reelection campaign is being hampered by stubbornly high prices and frozen wages, the ultimate economic phenomenon that makes consumers feel that the economy isn’t doing well.

President Biden’s reelection campaign is being hampered by stubbornly high prices and frozen wages, the ultimate economic phenomenon that makes consumers feel that the economy isn’t doing well.

Hi. Joe Biden here, asking for more money for Ukraine and Israel.

Many Americans are asking: why, while millions of Americans are unemployed and getting evicted and starving and homeless, should we ignore our own people and send billions of dollars to foreign countries instead? The answer is: democracy. We have to defend democracy.

Ukraine and Israel aren’t just democracies. They’re special democracies.

Very special democracies.

Ukraine, for example, is the kind of democracy that doesn’t hold elections for local offices. There were supposed to be parliamentary elections, this month, but…yeah. There weren’t and there won’t be. Don’t worry, it’s perfectly legal because after the war with Russia started in February 2022, martial law was declared and the Ukrainian Constitution doesn’t allow elections under martial law.

Ukraine is so democratic that it doesn’t even need to have presidential elections anymore. Martial law again. And who declared martial law? Why, it’s that sly rascal President Volodymyr Zelensky—make that President-for-Life Volodymyr Zelensky. We’re so dysfunctional here in the U.S. that House Republicans can’t agree with themselves who should be Speaker. But Ukraine is streamlined! The guy who would be running for reelection this spring won’t have to, because he personally said so! That’s a very special democracy.

Under “martial law,” a term that no one has ever managed to define, Ukraine is a kind of democracy in which “conducting referendums, organizing strikes, and holding public demonstrations and other mass gatherings are prohibited.” Special!

President-for-Life Zelensky points out: “according to the [martial law] legislation, it is forbidden to hold elections.” Legislation that he signed unilaterally, of course. He is so committed to the rule of law that he refuses to unilaterally cancel a law that he unilaterally created in order to cancel the rule of law.

As everyone knows, you don’t need to hold elections to call yourself a democracy. Aside from martial law, there would be some big logistical challenges to holding an election right now. Like, Zelensky could lose! In the last poll of Ukrainians before the war, 53% of voters disapproved of his job performance and 38% approved.

Also, an election without other candidates and parties isn’t much fun. Ukraine has banned all left-wing parties, and also banned 11 other parties, including the biggest one, whose leader is under house arrest. Better not to bother.

Even if there were other parties and candidates to run against Zelensky, which there are not, they wouldn’t be able to campaign because “conducting referendums, organizing strikes, and holding public demonstrations and other mass gatherings are prohibited” under martial law. Who needs campaign rallies, because who would report about them anyway? His Excellency the President-for-Life has imposed state censorship on newspapers, shuttered opposition websites and shut down all opposition TV outlets and consolidated them into his own state TV platform. He calls it a “unified information policy.” No more channel changing! Save on monthly subscriptions to media apps!

The U.S. spent over $14 billion on the 2020 election. Ukraine is a very efficient democracy. They’re spending nothing at all! We must defend this penny-pinching beacon of freedom.

Israel, I like to say, is “a safe, secure, Jewish, and democratic state.” OK, not that safe. But, like Ukraine, it’s a democracy. Israel is a very very special kind of democracy.

In a democracy, the right to vote is one of the most fundamental privileges accorded to a citizen. The trouble is, sometimes people vote incorrectly. And in a democracy, all you need to do to be considered a citizen is to be born and live in the country.

To fix this problem, Israel has decided that only its very best people—the 9.6 million residents of Israel “proper”—can be citizens. The 2.4 million Palestinians in Gaza or the 2.7 million Palestinians in the West Bank are, as the vernacular goes, S.O.L. (The 500,000 Israeli settler-colonists squatting in the West Bank are, however, fully vested voters.)

Of the 9.6 million Israelis in Israel proper, 2.0 million are Israeli Arabs and 500,000 are neither Jewish nor Arab. If they and the West Bank settlers voted alongside their fellow 5.1 million Arabs in Gaza and the West Bank in a unified Israeli-Palestinian state, there would be 7.6 million Jews almost tied with 7.1 million Arabs.

Too much democracy.

On the other hand, 5.1 million Palestinian citizens of their own viable nation-state in a two-state scenario would present a different problem. The Republic of Palestine would have a seat at the United Nations, embassies and consulates all over the world, foreign news bureaus. Journalists and tourists could freely come and go. Palestinian citizens would talk. They’d complain, even about Israel. I mean, they do that now—but people might pay attention and—God forbid—care!

So Israel has an à la carte democracy. They lock the Palestinians away in Gaza and the West Bank, out of sight and out of mind, stateless and hopeless and voiceless, under Israeli occupation but without the right to vote. The Jewish “majority” of Israel enjoys the Middle East’s only thriving democracy.

Imagine how cool it would be if we could do that here! Turn the flyover “red” states into an occupied stateless concentration camp without voting rights. The remainder, the coastal “blue” states, would become a liberal paradise. No more Trumpies. Abortion rights—back. E-vehicle charging stations everywhere.

Israel has biggified democracy!

So, my fellow Americans, please join me in supporting Ukraine and Israel, these two very special, very expensive democracies.

While you’re still allowed.

(Ted Rall (Twitter: @tedrall), the political cartoonist, columnist and graphic novelist, co-hosts the left-vs-right DMZ America podcast with fellow cartoonist Scott Stantis. You can support Ted’s hard-hitting political cartoons and columns and see his work first by sponsoring his work on Patreon.)

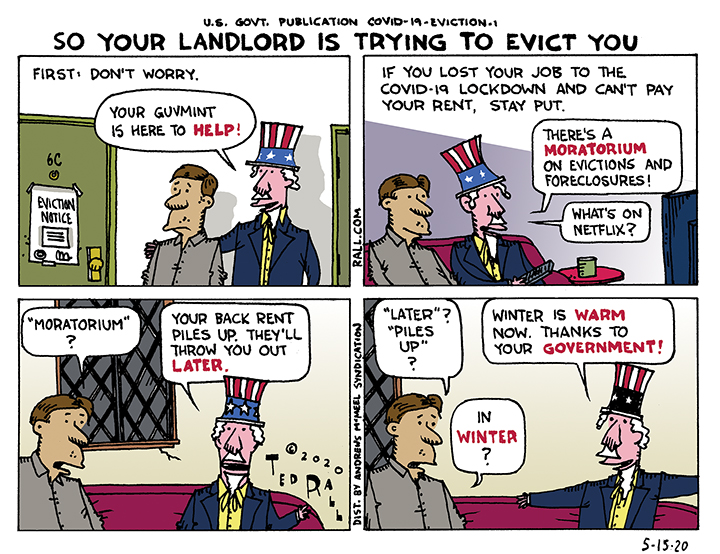

Voters will be going to the polls for the midterm elections six months from now. Democratic politicians know that they face an uphill climb and are likely to lose both the House of Representatives and the Senate. Yet the party hasn’t managed to coalesce behind a clear message beyond not being Republicans.

Biden’s response to the insanely low minimum wage, the ongoing healthcare crisis and the millions of people and businesses destroyed by the COVID-19 recession has been anemic; his defenders insist Trump was worse. But we can’t say “Trump was worse” when the rent is due.

Joe Biden is leading in the polls. Democrats would like to believe that things will get a lot better if he wins, but do they have any real basis to believe that?

Millions of Americans have lost their jobs, aren’t able to pay rent or their mortgages, and therefore face eviction or foreclosure. Yet the best that even “liberal” politicians are offering is a moratorium on evictions until some future point in time.

Odds are, you are poor. Or you’ve been poor.

Conventional wisdom — i.e., what the media says, not what most people think — repeatedly implies that poverty is a permanent state that chronically afflicts a relatively small number of Americans, while the rest of us thrive in a vast, if besieged, middle class. In fact, most Americans between age 25 and 75 have spent at least one year living under the poverty line.

“One of the biggest myths about poverty in the United States is that a relatively small segment of the population is poor, and that this represents a more or less permanent underclass,” Columbia University economist and social work professor Irwin Garfinkel tells Columbia magazine. “But poverty is quite dynamic. Lots of people move in and out of poverty over the course of their lives. And it doesn’t take much for people at the edge to lose their footing: a reduction in work hours, an inability to find affordable day care, a family breakup, or an illness — any of these can be disastrous.”

Even if you bounce back, the effects of these financial setbacks linger. For young adults, attending cheaper colleges or passing up higher education — or being unable to afford to take a low-paid internship — burdens them with opportunity costs that hobble them the remainder of their lives (which will likelier end sooner). Debts accrue with compound interest and must be repaid; damaged credit ratings block qualified buyers from purchasing homes. Diseases go undetected and untreated during periods without healthcare. Gaps on resumes are a red flag for employers.

Americans pay a price for the boom-and-bust cycle of capitalism. To find out exactly how high the cost is, Professor Garfinkel and his colleagues at Columbia have created the Poverty Tracker, dubbed “one of the most richly detailed studies of poverty ever undertaken in the United States.” The Poverty Tracker is “a meticulous long-term survey of 2,300 New York households across all income levels…for at least two years” that aims “to create a much more intimate and precise portrait of economic distress than has ever been conducted in any US city.”

Initial findings were distressing: “While the city’s official poverty rate is 21%, the Columbia researchers found that 37% of New Yorkers, or about 3 million people, went through an extended period in 2012 when money was so tight that they lost their home, had their utilities shut off, neglected to seek medical treatment for an illness, went hungry, or experienced another ‘severe material hardship,’ as the researchers define such extreme consequences.”

Wait, it’s even worse than that:

“Even the 37% figure understates the number of New Yorkers who endured tough times in 2012. The researchers estimate that two million more endured what they call ‘moderate material hardship,’ which, as opposed to, say, losing one’s home or having the lights shut off, might involve merely falling behind on the rent or utility bills for a couple of months. Many others were in poor health. Indeed, the researchers found that if you add together all of those who were in poverty, suffered severe material hardship, or had a serious health problem, this represented more than half of all New Yorkers [emphasis is mine].”

The researchers hope that “they will have enough data to begin helping public authorities, legislators, foundations, nonprofits, philanthropists, and private charities address the underlying problems that affect the city’s poor” by the end of 2014.

Nationally, more than 35% of all Americans are currently ducking calls from collection agencies over unpaid debts.

What can be done?

Under this system? Not much. Democrats, who haven’t even proposed a major anti-poverty program since the 1960s, aren’t meaningfully better on poverty than Republicans.

As things stand, the best we can hope for from the political classes are crumbs: a few teeny-weeny proposals for wee reforms.

Like expanding day-care programs. More school lunches. Housing subsidies. “Additional investments in food programs.”

A drop in the bucket in an ocean of misery.

The Poverty Tracker shows that poverty is a huge problem in the United States. Unfortunately its authors, who draw their salaries from an institution intimately intertwined with monied elites, dare not openly suggest what they know to be true, that the key to eliminating poverty is to get rid of its root cause: capitalism.

(Ted Rall, syndicated writer and cartoonist, is the author of “After We Kill You, We Will Welcome You Back As Honored Guests: Unembedded in Afghanistan,” out Sept. 2. Subscribe to Ted Rall at Beacon.)

COPYRIGHT 2014 TED RALL, DISTRIBUTED BY CREATORS.COM

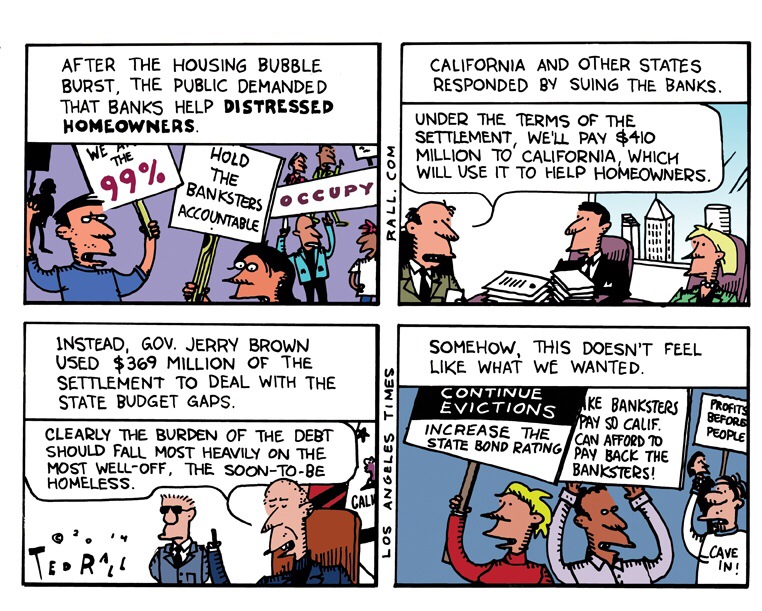

As a news junkie and student of the human condition, it takes a lot to make my blood come to a full boil. It takes even more to make me sympathize with wealthy corporations. Hand it to Gov. Jerry Brown — he managed to pull off both feats with the news that he diverted $350 million from California’s share of the 2012 national mortgage settlement in order to reduce the state’s 2013 budget deficit.

Now that California is enjoying a budget surplus, a coalition of homeowner advocates and religious organizations has filed suit against the state to force Brown to restore the money.

Back in 2008-09, the real estate bubble burst, taking the global economy with it. By many measures, especially real unemployment and median wages, we still haven’t recovered.

By 2010 a political consensus had formed. Though politicians were partly to blame, the worst offenders were the giant “too big to fail” banks that had knowingly approved loans to homebuyers who couldn’t afford to pay them back, sold bundles of junk mortgage derivatives to unsuspecting investors and secretly hedged their bets against their clients. After the house of cards came down, they played the other side. They cashed in their chips, refused to refinance mortgages even though interest rates had fallen and deployed “robo-signers” to illegally evict hundreds of thousands of homeowners — including people who had never missed a payment — to ding them with outrageous late fees on their way to profitable (for the banks) foreclosure.

On the Left, anger at the banks coalesced around the Occupy Wall Street movement. Though less widely reported, anti-bank sentiment also found a home in the Tea Party.

Politics ultimately play out in the courts. Lawsuits filed by state attorney generals forced the banks to the bargaining table. In 2012 they agreed to cough up $26 billion as penance.

The money was supposed to compensate people who had lost their homes and to help those who were hanging on by a thread avoid eviction, either by refinancing at lower rates or writing down principal to reflect lower real estate prices.

Enter the governors.

Jerry Brown wasn’t unique. Cash-hungry states siphoned off half of their share of the mortgage settlement to plug holes in their budgets.

We will never know how many families became homeless as a result.

The more you think about it, the more disgusting it is. Obviously it’s important for the state to get its fiscal house in order. But not at the expense of those least able to bear the burden. Desperate families lost — and are still losing — their homes so that holders of California’s state debt, much of it held by the same banks who caused the mortgage crisis, can be repaid.

This outrage is not without precedent.

Rather than the anti-smoking and health campaigns they were supposed to launch, the states siphoned off 47% of the $7.9 billion they received from the 1998 tobacco settlement for general budget purposes.

How many kids might have been reached by tobacco education programs that never got off the ground? How many will die of lung cancer? “Fifteen years after the tobacco settlement, our latest report finds that states are continuing to spend only a miniscule portion of their tobacco revenues to fight tobacco use,” the Campaign for Tobacco-Free Kids said in 2014. In Fiscal Year 2014, the states will collect $25 billion in revenue from the tobacco settlement and tobacco taxes, but will spend only 1.9 percent of it – $481.2 million – on programs to prevent kids from smoking and help smokers quit. This means the states are spending less than two cents of every dollar in tobacco revenue to fight tobacco use.”

This is the kind of behavior that prompts conservatives to characterize these settlements as government shakedowns of big business. It’s hard to disagree. As slimy as the banksters were and are — they’re sabotaging political solutions to the foreclosure crisis — they’re just greedy bastards doing what greedy bastards do. Public officials, on the other hand, are supposed to be on our side.

What Brown and his fellow governors have done with the mortgage settlement money is even more nauseating.

Why Aren’t Rioters Burning Down the Banks?

One in ten Americans take such antidepressants as Prozac and Paxil. Among those in their 40s and 50s, it’s 23%. Maybe that’s why we’re so passive.

Like the blissed-out soma-sucking drones of Huxley’s “Brave New World,” we must be too drugged to feel, much less express, rage. How else to explain that furious mobs haven’t burned the banks to the ground?

Last week, as the media ginned up empty speculation about Hillary Clinton’s presidential prospects, and wallowed in nuclear cognitive dissonance — Iran, which doesn’t have nukes and says it doesn’t want them, is repeatedly called a grave threat worth going to war over, while North Korea, which does have them and won’t stop threatening to turn the West Coast of the U.S. into a “sea of fire,” is dismissed as empty bluster, nothing to worry about — the Office of the Comptroller of the Currency and the Federal Reserve released the details of the settlement between the Obama Administration and the big banks over the illegal foreclosure scandal.

Citibank, JPMorgan Chase, Bank of America, Wells Fargo and other major home mortgage lenders foreclosed upon and evicted millions of homeowners between the start of the housing collapse in 2007 and 2011. Millions of families became homeless, including 2.3 million children. The vast majority of these Americans are still struggling; many fell into poverty from which they will never escape.

Disgusting, amazing, yet true: the banks had no legal right to evict these people. In many cases, the banks didn’t have basic paperwork, like the original deed to the house. They resorted to “robo-signing” boiler room operations to churn out falsified and forged eviction papers. In others cases, people could have kept their homes if they’d been allowed to refinance — their right under federal law — but the banks illegally refused, giving them the runaround, repeatedly asking for the same paperwork they’d already sent in. Soldiers fighting in Afghanistan and Iraq, protected from foreclosure under U.S. law, came home to find their homes resold at auction. In other cases, banks even repossessed homes where the homeowner had never missed a mortgage payment.

The foreclosure scandal helped spark the Occupy Wall Street movement.

Promising justice and compensation for the victims, President Obama’s Justice Department joined lawsuits filed by the attorneys general of several states.

Last year, Obama announced that the government had concluded a “landmark settlement” with the banks that would “deliver some measure of justice for those families that have been victims of their abusive practices.” The Politico newspaper called the $26 billion deal “a big win for the White House.” $26 billion. Sounds impressive, right?

So…the envelope, please.

How much will the banks have to pay? What will people whose homes were stolen — there is no other word — receive? Now we know the details.

Remember what we’re talking about. Your house is your biggest asset. You own tens of thousands, in some cases hundreds of thousands of dollars in equity. One morning the sheriff comes. He throws you and your family out on the street. Your possessions are dumped on the lawn. You have nowhere to go. Your kids are crying. If you were struggling before, now you’re completely screwed. And the bank that did it had no legal basis whatsoever to do what they did.

They took your house, sold it, and pocketed the profits.

What would happen to you if you walked into Tiffany’s and stole a $200,000 necklace?

The details:

So we’ve got more than 2.4 million families — that’s 5 million people — whose homes got bogarted by scumbag banksters. They’re getting a thousand bucks each on average. A thousand bucks for a two hundred thousand dollar theft! Not to mention the heartbreak and stress they suffered.

Why aren’t those five million people stringing up bank execs from telephone poles? It’s gotta be the Paxil.

But what really gets me is the 53 families who are getting $125,000 payouts for losing homes they were 100% up to date on.

Even if you’re a heartless right-winger, you’ve got to have a problem with a bank taking your house when you never missed a payment. Sorry, but these are multinational, multibillion dollar banks. They should pay these families tens of millions of dollars each.

Those 53 families should own Citibank, JPMorgan Chase, Bank of America and Wells Fargo.

Some perspective:

Citigroup CEO Vikram Pandit received $260 million in pay between 2007 and 2012, the height of the foreclosure scandal.

In 2011 alone, JPMorgan Chase CEO Jamie Dimon was given $23 million. In 2012, the company’s board of directors “punished” him for a $6 billion loss in derivatives trading by paying him “merely” $18.7 million.

In 2012 alone, Bank of America paid CEO Brian Moynihan $12 million; Wells Fargo paid $23 million to CEO John Stumpf.

Not bad for some of the worst criminals in history.

That’s how things work in the United States: the criminals get the big payouts. The people whose lives they destroy get $300.

(Ted Rall’s website is tedrall.com. His book “After We Kill You, We Will Welcome You Back As Honored Guests: Unembedded in Afghanistan” will be released in November by Farrar, Straus & Giroux.)

COPYRIGHT 2013 TED RALL