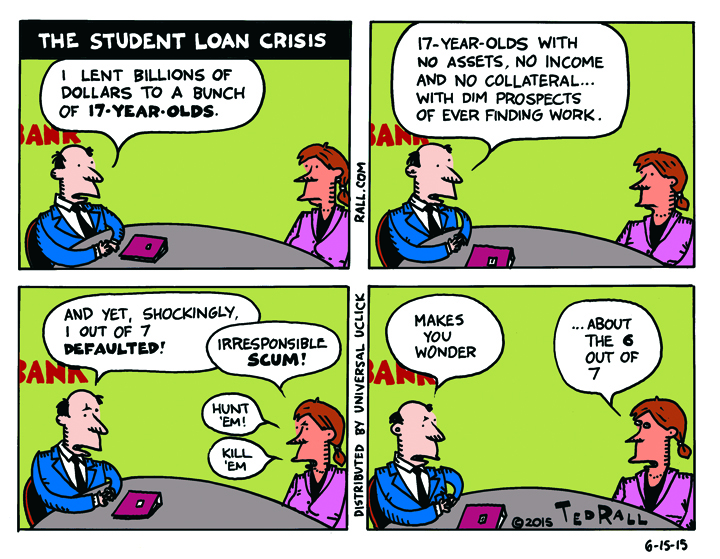

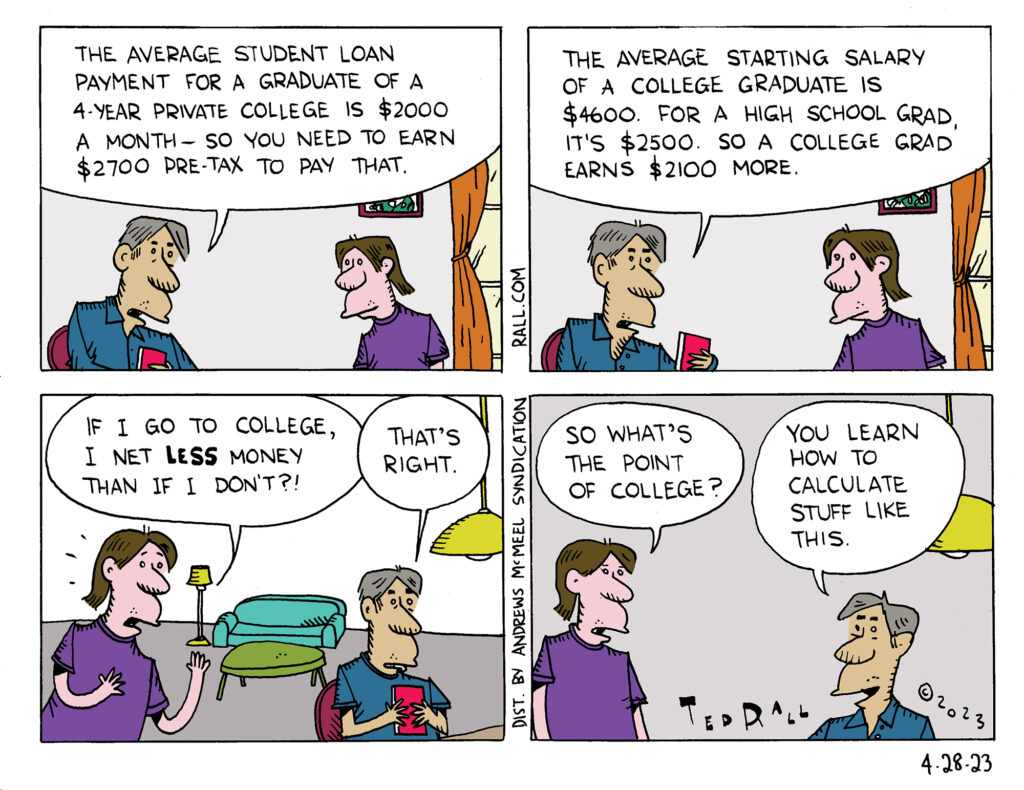

The “college premium”—the extra money you get from having a college degree compared to someone without one—has been eclipsed, more than eclipsed, by staggeringly high tuitions and resulting student loan burdens. There are still good reasons to go to college, but making more money probably isn’t one of them.