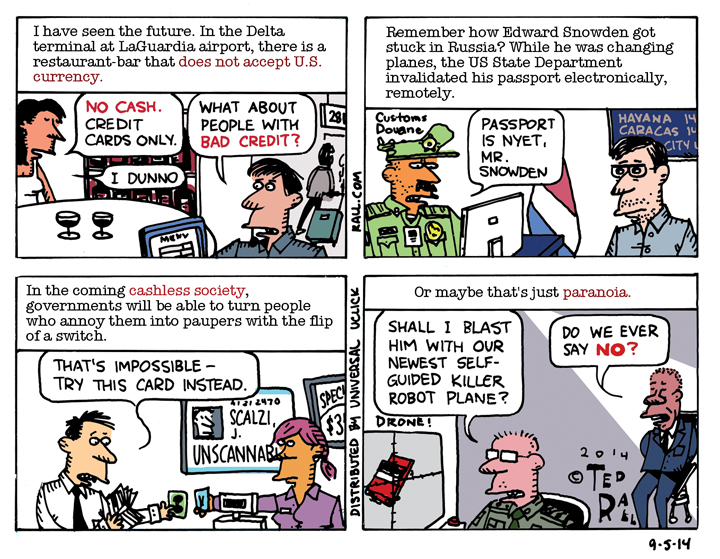

I live in New York City, where many homeless people rely on panhandling in order to get by. A few days ago I saw a Millennial woman turn down a request from a homeless man, saying, “I don’t carry cash.” I have long been concerned about the ramifications of our increasingly cashless society, like the ability of the government to lock down our bank accounts and ability to move freely. As usual, the poorest among us are paying the biggest price for what we’ve been told is progress.