The Cashless Society is Here

•

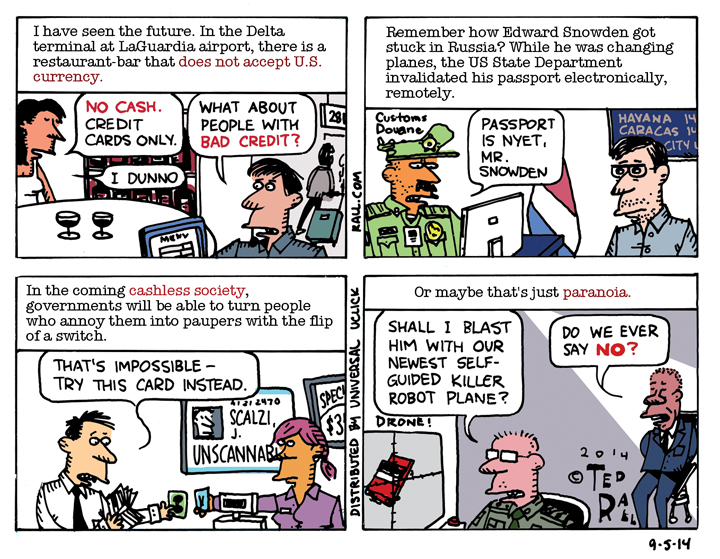

I have seen our future dystopian cashless society. What could go wrong? After all, it’s not the government would ever use its power to shut off people’s access to their money with a flip of a switch.

Diversify Your Criminality

•

An expensive luxury during a recession, states scaled back the war on drugs. Now that recovery has begun, look for more prisons and longer sentences to fill them.

SYNDICATED COLUMN: Another Obama Sellout

•

Mortgage Settlement a Sad Joke

Joe Nocera, the columnist currently challenging Tom Friedman for the title of Hackiest Militant Centrist Hack—it’s a tough job that just about everyone on The New York Times op-ed page has to do—loves the robo-signing settlement announced last week between the Obama Administration, 49 states and the five biggest mortgage banks. “Two cheers!” shouts Nocera.

Too busy to follow the news? Read Nocera. If he likes something, it’s probably stupid, evil, or both.

As penance for their sins—securitizing fraudulent mortgages, using forged deeds to foreclose on millions of Americans and oh, yeah, borking the entire world economy—Ally Financial, Bank of America, Citibank, JPMorgan Chase and Wells Fargo have agreed to fork over $5 billion in cash. Under the terms of the new agreement they’re supposed to reduce the principal of loans to homeowners who are “underwater” on their mortgages—i.e. they owe more than their house is worth—by $17 billion.

Some homeowners will qualify for $3 billion in interest refinancing, something the banks have resisted since the ongoing depression began in late 2008.

What about those who got kicked out of their homes illegally? They split a pool of $1.5 billion.

Sounds impressive. It’s not. Mark Zuckerberg is worth $45 billion.

“That probably nets out to less than $2,000 a person,” notes The Times. “There’s no doubt that the banks are happy with this deal. You would be, too, if your bill for lying to courts and end-running the law came to less than $2,000 per loan file.”

Readers will recall that I paid more than that for a speeding ticket. 68 in a 55.

This is the latest sellout by a corrupt system that would rather line the pockets of felonious bankers than put them where they belong: prison.

Remember TARP, the initial bailout? Democrats and Republicans, George W. Bush and Barack Obama agreed to dole out $700 billion in public—plus $7.7 trillion funneled secretly through the Fed—to the big banks so they could “increase their lending in order to loosen credit markets,” in the words of Senator Olympia Snowe, a Maine Republican.

Never happened.

Three years after TARP “tight home loan credit is affecting everything from home sales to household finances,” USA Today reported. “Many borrowers are struggling to qualify for loans to buy homes…Those who can get loans need higher credit scores and bigger down payments than they would have in recent years. They face more demands to prove their incomes, verify assets, show steady employment and explain things such as new credit cards and small bank account deposits. Even then, they may not qualify for the lowest interest rates.”

Financial experts aren’t surprised. TARP was a no-strings-attached deal devoid of any requirement that banks increase lending. You can hardly blame the bankers for taking advantage. They used the cash—money that might have been used to help distressed homeowners—to grow income on their overnight “float” and issue record raises to their CEOs.

Next came Obama’s “Home Affordable Modification Program” farce. Another toothless “voluntary” program, HAMP asked banks to do the same things they’ve just agreed to under the robo-signing settlement: allow homeowners who are struggling to refinance and possibly reduce their principals to reflect the collapse of housing prices in most markets.

Voluntary = worthless.

CNN reported on January 24th: “The HAMP program, which was designed to lower troubled borrowers’ mortgage rates to no more than 31% of their monthly income, ran into problems almost immediately. Many lenders lost documents, and many borrowers didn’t qualify. Three years later, it has helped a scant 910,000 homeowners—a far cry from the promised 4 million.”

Or the 15 million who needed help.

As usual, state-controlled media is too kind. Banks didn’t “lose” documents. They threw them away.

One hopes they recycled.

I wrote about my experience with HAMP: Chase Home Mortgage repeatedly asked for, received, confirmed receiving, then requested the same documents. They elevated the runaround to an art. My favorite part was how Chase wouldn’t respond to queries for a month, then request the bank statement for that month. They did this over and over. The final result: losing half my income “did not represent income loss.”

It’s simple math: in 67 percent of cases, banks make more money through foreclosure than working to keep families in their homes.

This time is different, claims the White House. “No more lost paperwork, no more excuses, no more runaround,” HUD secretary Shaun Donovan said February 9th. The new standards will “force the banks to clean up their acts.”

Don’t bet on it. The Administration promises “a robust enforcement mechanism”—i.e. an independent monitor. Such an agency, which would supervise the handling of million of distressed homeowners, won’t be able to handle the workload according to mortgage experts. Anyway, it’s not like there isn’t already a law. Law Professor Alan White of Valparaiso University notes: “Much of this [agreement] is restating obligations loan servicers already have.”

Finally, there’s the issue of fairness. “Underwater” is a scary, headline-grabbing word. But it doesn’t tell the whole story.

Tens of millions of homeowners have seen the value of their homes plummet since the housing crash. (The average home price fell from $270,000 in 2006 to $165,000 in 2011.) Those who are underwater tended not to have had much equity in their homes in the first place, having put down low downpayments. Why single them out for special assistance? Shouldn’t people who owned their homes free and clear and those who had significant equity at the beginning of crisis get as much help as those who lost less in the first place? What about renters? Why should people who were well-off enough to afford to buy a home get a payoff ahead of poor renters?

The biggest fairness issue of all, of course, is one of simple justice. If you steal someone’s house, you should go to jail. If your crimes are company policy, that company should be nationalized or forced out of business.

Your victim should get his or her house back, plus interest and penalties.

You shouldn’t pay less than a speeding ticket for stealing a house.

(Ted Rall is the author of “The Anti-American Manifesto.” His website is tedrall.com.)

COPYRIGHT 2012 TED RALL

SYNDICATED COLUMN: Toxic Assets

•

Many Foreclosed Houses Are Infested by Mold

The next time someone tells you that capitalism is efficient, remember the mold houses.

I used to be a banker. Some of my customers had trouble making their loan payments. We usually had recourse to some sort of collateral—often real estate. But my bank really didn’t want to foreclose.

“We’re bankers,” my boss told me the first time this issue came up. “Not landlords.”

Back in the 1980s most banks held this view. Bankers sat on their butts in air-conditioned offices. They didn’t want to manage vacated properties, much less try to sell them. They understood banking. Banking was a straightforward business: take deposits, issue loans, collect the difference in interest as profit.

It was boring. Just the way they liked it.

My bank did a lot to avoid declaring a default. We lowered interest rates. We allowed skipped payments. Sometimes we even reduced principal.

Banking became exciting during the 1990s. Glass-Steagall got repealed, allowing formerly staid bankers to compete with high-flying Wall Street financiers in the securities business. Bank consulting firms invented big new fees for services that used to be free, like using an ATM.

Banks issued millions of home loans to borrowers whom they knew couldn’t afford to pay them back. Crédit Suisse estimates that such “liars’ loans” accounted for 49 percent of originations by 2006. Why they’d do it? Like mobsters, bank executives were “busting out” their companies—generating false short-term profits in order to collect annual performance bonuses. By the time the toxic chickens came home to roost, as they did in the form of the September 2008 financial crisis, they and their paychecks had moved on.

As the global financial system was in the midst of total collapse, greedy bankers conjured up a way to profit from the very misery they had caused. Rather than work with distressed homeowners who faced foreclosure (for example, refinancing subprime and adjustable rate mortgages into old-fashioned 30-year fixed mortgages) they dragged out the process in order to collect more late fees.

Banks were eager to foreclose. They were merciless. They evicted homeowners while they were on active-duty serving in Iraq and Afghanistan, a violation of federal law. They even evicted people who didn’t owe them a cent.

Now banks are sitting on top of nearly a million homes. “All told, [banks] own more than 872,000 homes as a result of the groundswell in foreclosures, almost twice as many as when the financial crisis began in 2007, according to RealtyTrac, a real estate data provider,” reports The New York Times. “In addition, they are in the process of foreclosing on an additional one million homes and are poised to take possession of several million more in the years ahead.”

Which is where the wonderful tragic tale of the mold houses comes in.

“In most homes,” reported NPR recently, “as residents go in and out and the seasons change, natural ventilation sucks moisture up to the attic and out through the roof. It’s called the ‘stack effect.’ And in many parts of the country, it’s driven by air conditioning in the summer and heat in the winter. But no one is going in or out of most foreclosed homes—regardless of climate—and the effects can be devastating.”

Far from the profit center imagined by freshly-minted analysts with MBAs, empty houses depreciate faster than a new car driving off the lot. They fall apart quickly. Mildew and mold sets in, some of it toxic.

“In some states, it’s estimated that more than half of foreclosed homes have mold and mildew issues,” reported NPR. “Realtors across the country say they’re seeing the problem in everything from bungalows to mansions.”

Turns out those old-fashioned bankers were on to something. Bankers shouldn’t become landlords.

A minor mold problem starts at $5,000 and can easily run $20,000 or more. Considering that the average house in the Midwest is valued at $136,000, that’s not insignificant. Many houses with toxic mold have to be demolished.

Greed may be good. But it doesn’t always pay.

(Ted Rall is the author of “The Anti-American Manifesto.” His website is tedrall.com.)

COPYRIGHT 2011 TED RALL

Nothing New Here

•

The managing director of the International Monetary Fund has been charged with rape. What’s new? The IMF has been raping Third Worlders for years.

NEW WEBISODE: “Disposable” Episode #2

•

It’s out! The second official webisode (animated cartoon) by David Essman and yours truly about the downward slide of a typical American family living during the Obama Depression.

This time: Dan and Sarah attempt to hang on to their home.

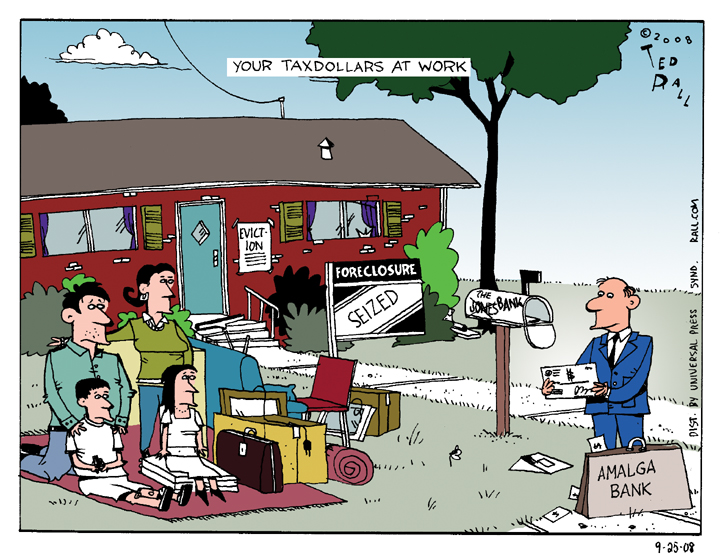

Your Taxdollars at Work

•

People need help. Banks get it instead. The only nice part is, it’s interesting to see rank capitalism, and its perverse relationship with government, exposed in all its glory.